高盛:2025年全球宏观经济及市场展望报告(深度解析)

Global Economics Analyst Macro Outlook 2025 Tailwinds (Probably) Trump Tariffs

We expect the second Trump administration to bring higher China and auto tariffs, much lower immigration, some fresh tax cuts, and regulatory easing. If so, the US economy should grow 2.5% in 2025, outperforming consensus expectations and other DM economies for the third year in a row. The biggest risk is a large across-the-board tariff, which would likely hit growth hard.

We have cut our Euro area GDP forecast to a below-consensus 0.8%, reflecting ongoing structural headwinds and a hit from trade policy uncertainty. We have also shaved our 2025 China GDP forecast to 4.5% because of higher US tariffs that are only partially offset by easier macro policies. Risks in both Europe and China are on the downside if tariffs increase beyond our baseline.

US core PCE inflation should slow to 2.4% by late 2025, higher than our prior forecast of 2.0% but still benign. Our forecast would rise to around 3% with an across-the-board tariff of 10%. In the Euro area, we expect core inflation to slow to 2% by late 2025 and are less concerned about upside risks even with a broader trade war. Lowflation risks have abated in Japan.

2025年宏观展望:利好因素(可能)胜过关税压力

我们预计,第二届特朗普政府可能会对中国商品和汽车征收更高的关税,大幅减少移民政策,推出一些新的减税措施,并进一步放松监管。在这种情况下,美国经济有望在2025年实现2.5%的增长,连续第三年超出市场共识预期,并优于其他发达经济体(DM)。然而,全面性高额关税构成最大的风险,可能对经济增长造成严重打击。

我们将欧元区GDP增长预测下调至0.8%(低于市场共识),这一调整反映了持续的结构性挑战以及贸易政策不确定性的影响。同样,我们将2025年中国GDP增长预测下调至4.5%,主要原因是更高的美国关税。尽管中国通过宽松的宏观政策部分缓解了关税的影响,但效果有限。如果关税规模超出我们的基线情景,欧洲和中国的经济下行风险将更加显著。

在通胀方面,我们预计到2025年底,美国核心个人消费支出(PCE)通胀率将放缓至2.4%,高于此前的预测值(2.0%),但仍处于温和水平。然而,若实施全面10%的关税,通胀率可能升至3%左右。在欧元区,我们预计核心通胀率到2025年底将下降至2%。即使更广泛的贸易战发生,我们对通胀上行的担忧仍相对有限。同时,日本的低通胀风险已基本消退。

We expect significant further rate cuts over the next year. The Fed is likely to cut to 3.25-3.5%, with sequential moves through Q1 and a slowdown thereafter. We have shaved our ECB forecast to 1.75% on the back of our growth downgrade and also see significant room for policy easing in EMs. However, we expect the Bank of Japan to lift its policy rate to 0.75% by year-end.

Our baseline forecast implies a benign risk backdrop and US outperformance. We expect modest positive returns across equities, commodities, and DM bonds, alongside gradual USD appreciation. But markets have already moved a long way in a risk-positive direction, and it will be important to limit exposure to the tails around our baseline.

Moving toward a broader trade war would reinforce USD upside but put pressure on global equities. Unusually high US equity valuations not only dampen long-term expected returns but also amplify the potential reaction to any economic weakness. By contrast, positive tailwinds could emerge if policies shift to be even more corporate friendly, oil prices fall more sharply on spare capacity, or inflation and fiscal fears prove overdone.

全球货币政策与市场展望

我们预计未来一年将出现显著的进一步降息。美联储可能在第一季度连续降息,将政策利率降至3.25%-3.5%,随后降息步伐放缓。基于我们对经济增长的下调预测,我们已将欧洲央行(ECB)的终端利率预测下调至1.75%,同时认为新兴市场(EM)仍有较大的政策宽松空间。然而,日本央行(BoJ)预计将在年底前将政策利率提高至0.75%。

我们的基线预测反映出风险环境总体温和,并预示美国经济表现持续领先。我们预计,股票、大宗商品和发达市场(DM)债券将实现温和正回报,同时美元(USD)将逐步升值。然而,市场已经在很大程度上反映了这种风险偏好的趋势,因此在基线预测的尾部风险上保持谨慎尤为重要。

全面贸易战的风险可能进一步推动美元走强,但会给全球股市带来压力。美国股市的高估值不仅压低了长期预期回报,还可能加剧对任何经济疲软的敏感反应。相比之下,如果政策转向更有利于企业,或油价因过剩产能显著下跌,又或者市场对通胀和财政风险的担忧被证明过度,则可能出现积极的利好因素。

The economic data this year have reinforced our long-standing optimism about post-pandemic normalization. Global GDP growth is tracking at 2.7% in 2024, similar to the 2023 pace and slightly above our estimate of potential, with US growth again leading the way among DMs. Global labor markets have rebalanced, with both unemployment and broader measures such as our jobs-workers gap back to pre-pandemic levels. Inflation has continued to trend down and is now within striking distance of central bank targets. And most central banks are well into the process of cutting interest rates back to more normal levels.

今年的经济数据进一步强化了我们对疫情后经济正常化的长期乐观预期。2024年全球GDP增长率预计为2.7%,与2023年的增速相当,略高于我们对潜在增长率的估计值,其中美国经济增长再次在发达市场(DM)中领跑。

全球劳动力市场已实现再平衡,失业率和“职位-工人缺口”等广义指标均恢复至疫情前的水平。通胀持续下降,目前已接近各国央行的目标范围。同时,大多数央行已深入推进降息进程,努力将利率恢复至更加常规的水平。

Trumponomics 2.0…

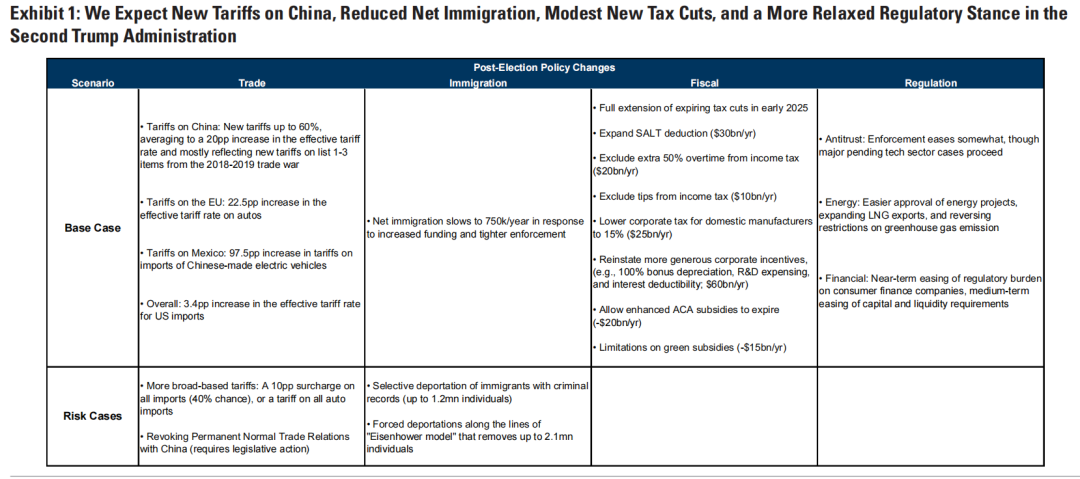

How will US economic policy change in the second Trump administration? Exhibit 1 summarizes our expectations for four areas of focus: trade, immigration, fiscal, and regulation.

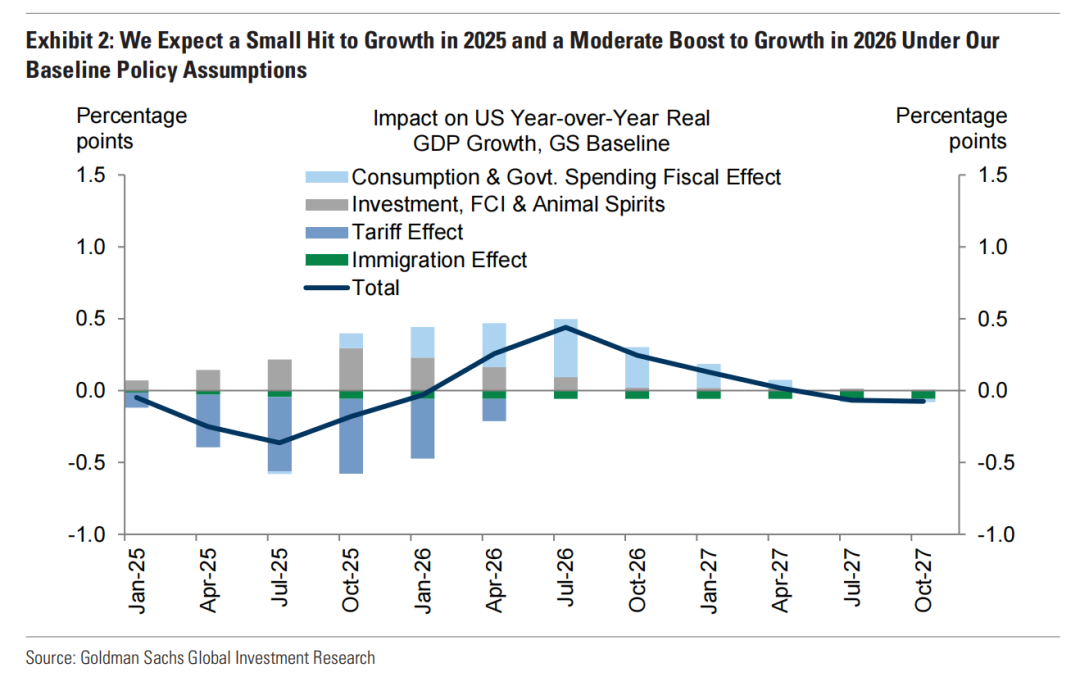

Exhibit 2 shows the effects on US GDP growth under our base case across all policies, while Exhibit 3 shows the effects for our risk case in which President-elect Trump imposes an across-the-board tariff of 10%. If this happens, the most likely timing is 2025H2. This means that there will likely be a period of uncertainty that may tighten financial conditions and weigh on growth. In our base case, the uncertainty resolves and financial conditions ease anew. In our tariff risk case, the uncertainty continues to build and financial conditions tighten further.

特朗普经济学2.0:政策变化的可能路径

第二届特朗普政府将如何调整美国的经济政策?我们在图表1中总结了四个重点领域的预期变化:贸易、移民、财政政策和监管。

图表2展示了基线情景下各项政策对美国GDP增长的影响,而图表3则显示了风险情景的影响——即特朗普总统实施10%的全面关税的情况。如果这一情景发生,最可能的时间是在2025年下半年。这将导致一段充满不确定性的时期,可能收紧金融环境并对经济增长造成压力。

在我们的基线情景中,这种不确定性最终将得到解决,金融环境也会重新放松。然而,在关税风险情景下,不确定性可能会持续加剧,金融环境进一步收紧,对经济的负面影响将更加显著。

The effects from the new policies on US GDP are small and largely offsetting under our baseline outlook. The new administration is likely to announce the China and auto tariffs relatively soon after the January 20 inauguration, which could also fuel uncertainty about broader tariff measures among businesses and market participants. These tariffs would result in a modest hit to real disposable personal income via higher consumer prices, and the broader uncertainty of how much further the trade war might escalate is likely to weigh on business investment. The result is a net drag averaging 0.2pp in 2025. Assuming that the trade war does not escalate further, we expect the positive impulses from tax cuts, a friendlier regulatory environment, and improved “animal spirits” among businesses to dominate in 2026, with a net boost to growth averaging 0.3pp.

在我们的基线预测中,新政策对美国GDP的影响较小,且大体上相互抵消。新一届政府可能会在1月20日就职后不久宣布针对中国商品和汽车的关税,这可能加剧企业和市场参与者对更广泛关税措施的不确定性。这些关税将通过更高的消费价格对实际可支配个人收入造成一定冲击,同时,贸易战可能进一步升级的不确定性可能抑制企业投资。

综合来看,这些因素预计将在2025年对经济增长造成平均0.2个百分点的拖累。假设贸易战没有进一步升级,我们预计减税、更友好的监管环境,以及企业更加积极的“动物精神”(市场信心)的正面推动力将在2026年占据主导地位,为经济增长平均带来0.3个百分点的提振。

In our tariff risk case, by contrast, the modest negative impulse from the China and auto tariffs gives way to a bigger negative impulse from the across-the-board tariff, both because the hit to real income increases and because trade policy uncertainty builds further. In 2026, this results in a net drag on growth averaging 1.0pp and peaking at 1.2pp, although the peak drag declines to 0.8pp if we assume that the increased tariff revenue is fully recycled into tax cuts.

与基线情景相比,在关税风险情景下,来自中国商品和汽车关税的温和负面冲击将被全面关税带来的更大负面影响取代。这种影响不仅体现在对实际收入的更大压缩,还表现在贸易政策不确定性的进一步加剧。

到2026年,这一情景预计对经济增长的平均拖累达1.0个百分点,并在峰值时达到1.2个百分点。然而,如果假设新增的关税收入全部用于减税,峰值拖累可减轻至0.8个百分点。

…And Its Effects on Europe and China

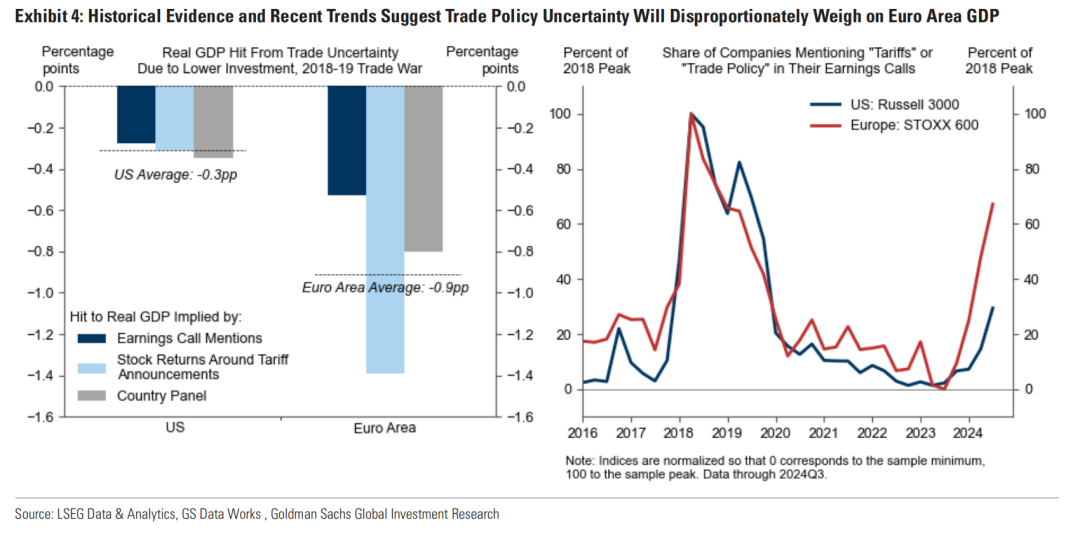

The growth hit from US trade policy is greater elsewhere. One key finding in our research on tariffs is the important impact of trade policy uncertainty (TPU) on growth in the Euro area. The left chart in Exhibit 4 summarizes research suggesting that a rise in TPU to the peak levels of the 2018-19 trade war would subtract 0.3% from GDP in the US but as much as 0.9% in the Euro area. Moreover, the right chart shows that trade policy uncertainty (measured via mentions in corporate earnings reports) has already risen much more in the Euro area than in the US. We therefore cut our 2025 Euro area growth forecast on the back of the US election results by 0.5pp on a Q4/Q4 basis and would likely cut it further if the US imposes an across-the-board tariff.

对欧洲和中国的影响

美国贸易政策对其他地区的经济增长打击更为显著。我们的关税研究揭示了贸易政策不确定性(TPU)对欧元区增长的重要影响。在图表4的左图中,研究结果表明,TPU上升至2018-19年贸易战的峰值水平时,美国GDP将减少0.3%,而欧元区GDP的降幅可能高达0.9%。此外,右图显示,贸易政策不确定性(通过企业财报中相关提及次数衡量)在欧元区的上升幅度已显著高于美国。

基于美国大选结果带来的影响,我们将2025年欧元区增长预测的Q4/Q4增速下调了0.5个百分点。如果美国实施全面关税,我们可能还会进一步下调欧元区的增长预测。

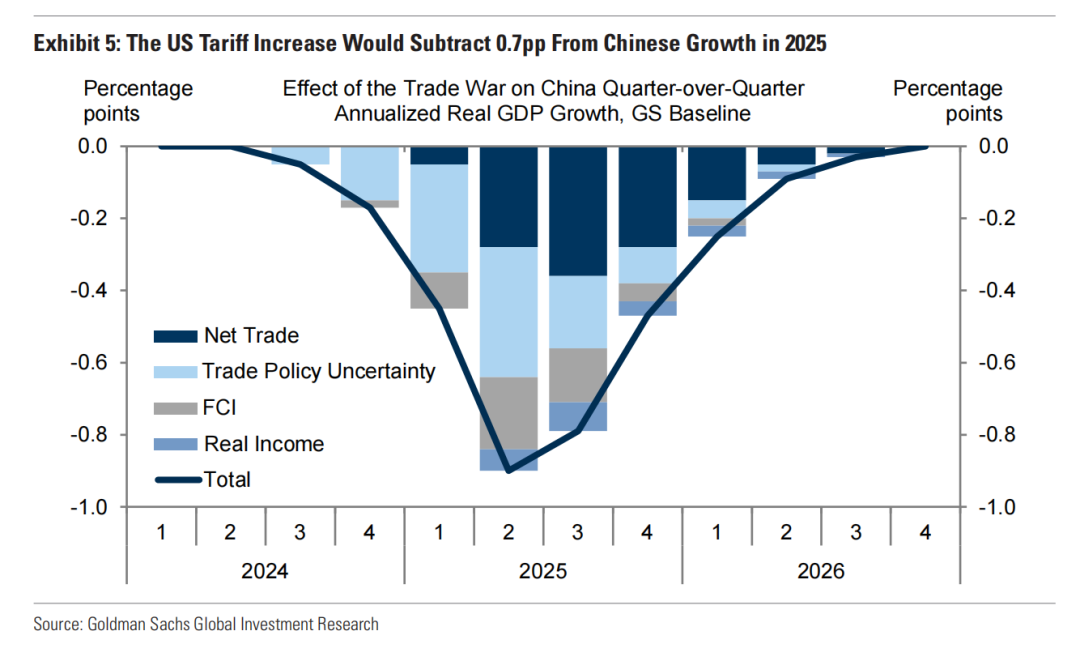

The impact is more direct in China, which will almost certainly face tariff increases that we expect will reach up to 60pp and average 20pp across all exports to the US. As shown in Exhibit 5, we estimate that the US tariff increase in our baseline scenario will subtract almost 0.7pp from China growth in 2025. Assuming that Chinese policymakers provide macro stimulus and some of the growth hit is offset by RMB depreciation, we have cut our 2025 growth forecast more modestly, by 0.2pp on net to 4.5%. However, we would likely make larger downgrades if the trade war were to escalate further, either with an across-the-board tariff or more aggressive China-specific measures such as an end to permanent normal trade relations (PNTR) between the US and China.

对中国的直接影响

相比其他地区,中国受到的影响更加直接。中国几乎可以肯定将面临关税上调,我们预计关税增幅可能高达60个百分点,平均对所有出口至美国的商品征收约20个百分点的关税。如图表5所示,在我们的基线情景中,美国关税的上调预计将在2025年削减中国经济增长近0.7个百分点。

考虑到中国政府可能通过宏观刺激政策应对,以及人民币贬值在一定程度上抵消了部分冲击,我们对2025年中国经济增长的预测进行了相对温和的下调,仅削减0.2个百分点,至4.5%。然而,如果贸易战进一步升级,例如实施全面关税或采取更具针对性的措施(如终止中美之间的永久正常贸易关系 PNTR),我们可能会进行更大幅度的预测下调。

We also expect a drag from US trade policy in other economies, with larger drags in more trade-exposed economies and potential boosts in certain EMs that are well positioned to gain export share if trade shifts away from China (e.g., Mexico and Vietnam). Overall, we estimate changes to US trade policy will subtract 0.4% from global GDP, although increased policy support should dampen this hit. The impact could be 2-3 times larger if the US imposes a 10% across-the-board tariff.

美国贸易政策对其他经济体的影响

我们预计,美国贸易政策还会对其他经济体造成拖累,对贸易依赖程度更高的经济体的影响更大。与此同时,一些新兴市场(EM)国家可能因贸易从中国转移而获得出口份额的提升,例如墨西哥和越南。

整体来看,估计美国贸易政策的变化将导致全球GDP下降0.4%,尽管政策支持的增加可能在一定程度上缓解这一影响。如果美国实施10%的全面关税,其影响可能扩大至2-3倍。

Modest Price Boosts from Tariffs

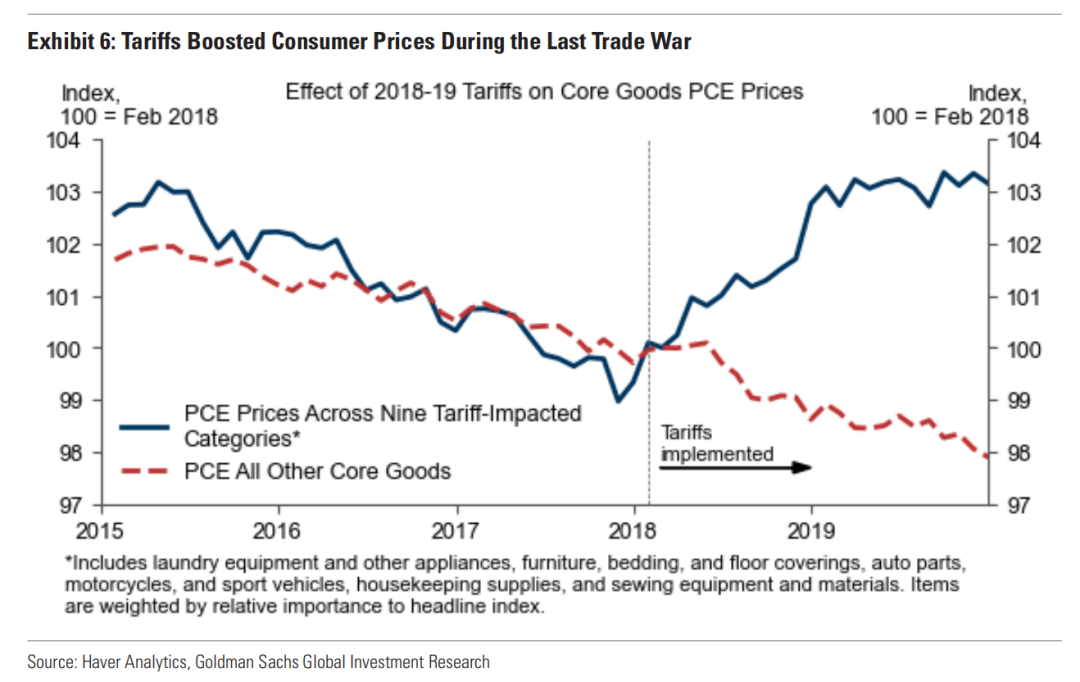

Higher tariffs will also raise US inflation, at least in the short term. The experience of the first Trump administration shows that tariffs are largely passed on to consumer prices. This is visible in the fact that prices in tariffed PCE categories rose by almost exactly the tariff amount, while prices in non-tariffed categories remained on their prior trend (Exhibit 6).

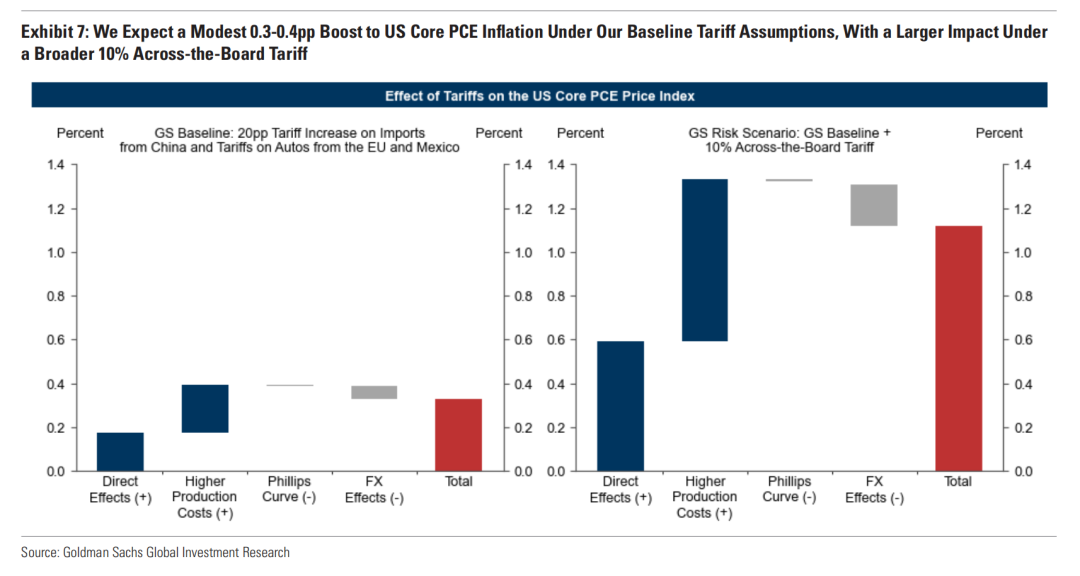

If tariffs are confined to China and autos from Europe and Mexico, this analysis implies that the US inflation impact will be a relatively modest 0.3-0.4pp, as shown in Exhibit 7. If we add a broader 10% across-the-board tariff, the impact rises to almost 1.2pp. Barring significant second-round effects via expectations or wages, however, tariff effects are price level effects, so the inflation impact subsides in 2026-2027. Outside the US, inflation effects should be minor even under our assumption of full retaliation.

关税引发的温和价格上涨

更高的关税将在短期内推动美国通胀上升。第一届特朗普政府的经验表明,关税的成本大部分转嫁到了消费者价格上。这一点可以从数据中看出:征收关税的个人消费支出(PCE)类别价格几乎完全按关税幅度上升,而未征收关税的类别价格则保持原有趋势(见图表6)。

如果关税仅限于中国商品以及来自欧洲和墨西哥的汽车,本分析表明其对美国通胀的影响相对温和,约为0.3-0.4个百分点(见图表7)。但如果加征全面10%的关税,通胀的影响可能升至近1.2个百分点。然而,若无通过预期或工资产生的显著次轮效应,关税的影响主要是价格水平效应,因此预计通胀影响将在2026-2027年逐渐消退。

在美国以外的地区,即使假设全面报复性措施,通胀影响预计仍较小。

Another Solid Year for Global Growth

The upshot is that, barring a broader trade war, policy changes in the second Trump administration are unlikely to change the broad contours of our global economic views.

As shown in Exhibit 8, we expect global growth to average 2.7% in 2025, nearly the same pace as in 2024 and slightly above consensus. Relative to consensus, we are optimistic in the US and pessimistic in the Euro area, with other major economies in between.

A key reason for optimism on global growth is the dramatic inflation decline over the past two years. This directly supports real income because price inflation has fallen far more quickly than wage inflation, which is still elevated as workers make up for the real wage losses they suffered in the early post-pandemic years. The resulting strength in real hourly wages has helped real disposable household income grow 3-4% over the past year across the major advanced economies, a pace that is likely to moderate in Europe but should remain strong in the US and Canada in 2025 (Exhibit 9).

全球增长再迎稳健一年

总体而言,只要不发生更大范围的贸易战,第二届特朗普政府的政策变化预计不会显著改变我们对全球经济的整体看法。

正如图表8所示,我们预计2025年全球经济增长率将平均达到2.7%,与2024年的增速几乎持平,且略高于市场共识。相较于市场预期,我们对美国经济持乐观态度,对欧元区则偏悲观,其他主要经济体的预期介于两者之间。

支撑全球经济增长的一个关键因素是过去两年通胀水平的大幅下降。这一趋势直接提升了实际收入,因为价格通胀的下降速度显著快于工资通胀,而工资通胀仍处于较高水平,反映了劳动力为弥补疫情后实际工资损失所进行的调整。这种趋势带来了实际小时工资的增长,从而推动了主要发达经济体过去一年实际可支配家庭收入增长了3-4%。尽管这种增速在欧洲可能会有所放缓,但在美国和加拿大预计将在2025年保持强劲(见图表9)。

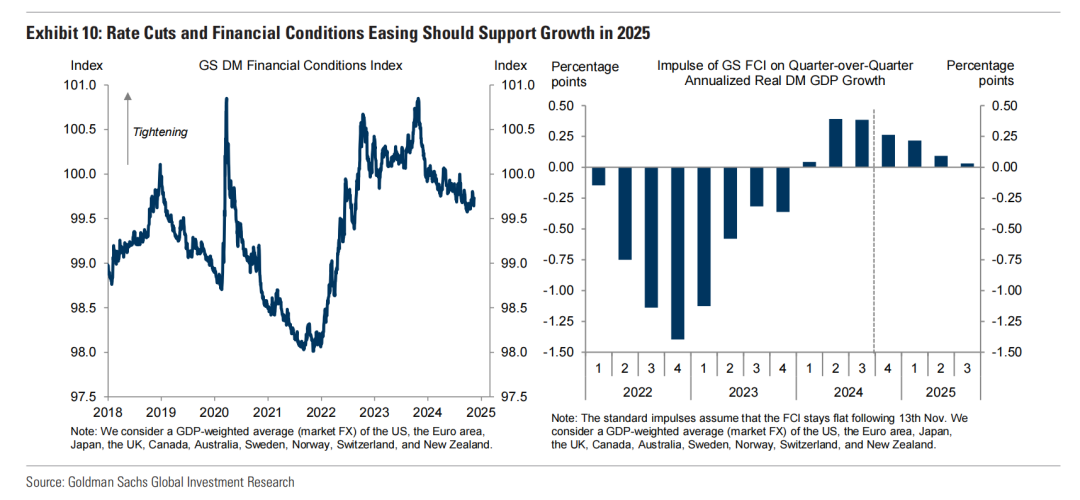

Just as importantly, the inflation decline also indirectly supports demand by allowing central banks to normalize monetary policy and thereby ease financial conditions. Under the simplifying assumption that our financial conditions indices remain at their latest spot level, we estimate a positive impulse to growth of about 0.2pp across the G10 economies over the next four quarters (Exhibit 10). If financial conditions ease further on the back of solid global growth and central bank policy rate cuts, the positive impulse would be greater.

同样重要的是,通胀的下降还通过允许央行正常化货币政策并从而缓解金融环境,间接支持了需求。在假设我们的金融条件指数保持在当前水平不变的情况下,我们估算未来四个季度,G10经济体将因此获得约0.2个百分点的增长正向推动力(见图表10)。如果全球增长强劲且央行进一步下调政策利率从而进一步缓解金融条件,那么这一正向推动力将更为显著。

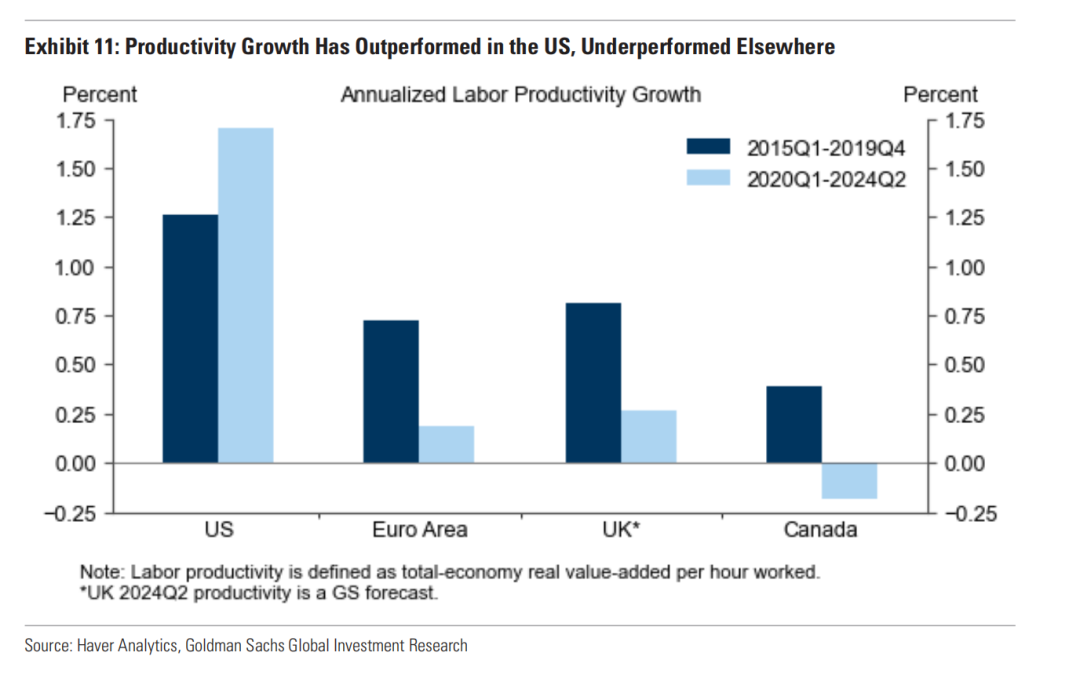

None of this explains why real GDP is growing so much faster in the US than in other advanced economies. The answer, instead, is found on the supply side. Following the recent revisions to the US national accounts, labor productivity in the US has grown at a 1.7% annualized rate since late 2019, a clear acceleration from the pre-pandemic trend of 1.3%. By contrast, labor productivity in the Euro area has grown at a 0.2% annualized rate over the same period, a clear deceleration from an already-mediocre 0.7% before the pandemic. Other advanced economies have shown similarly lackluster trends (Exhibit 11). We expect US productivity growth to remain significantly stronger than elsewhere, and this is a key reason why we expect US GDP growth to continue to outperform.

为何美国实际GDP增速远超其他发达经济体?

这一现象并非由需求侧因素解释,而是可以从供给侧找到答案。根据最近对美国国家账户数据的修订,自2019年底以来,美国的劳动生产率年化增速达到了1.7%,明显快于疫情前1.3%的增长趋势。相比之下,欧元区劳动生产率同期仅实现了0.2%的年化增速,远低于疫情前已显平庸的0.7%水平。其他发达经济体的表现也同样乏力(见图表11)。

我们预计,美国的生产率增长将持续显著高于其他经济体,这是我们预期美国GDP增长继续领先的一个关键原因。

Remember Bumpy Disinflation?

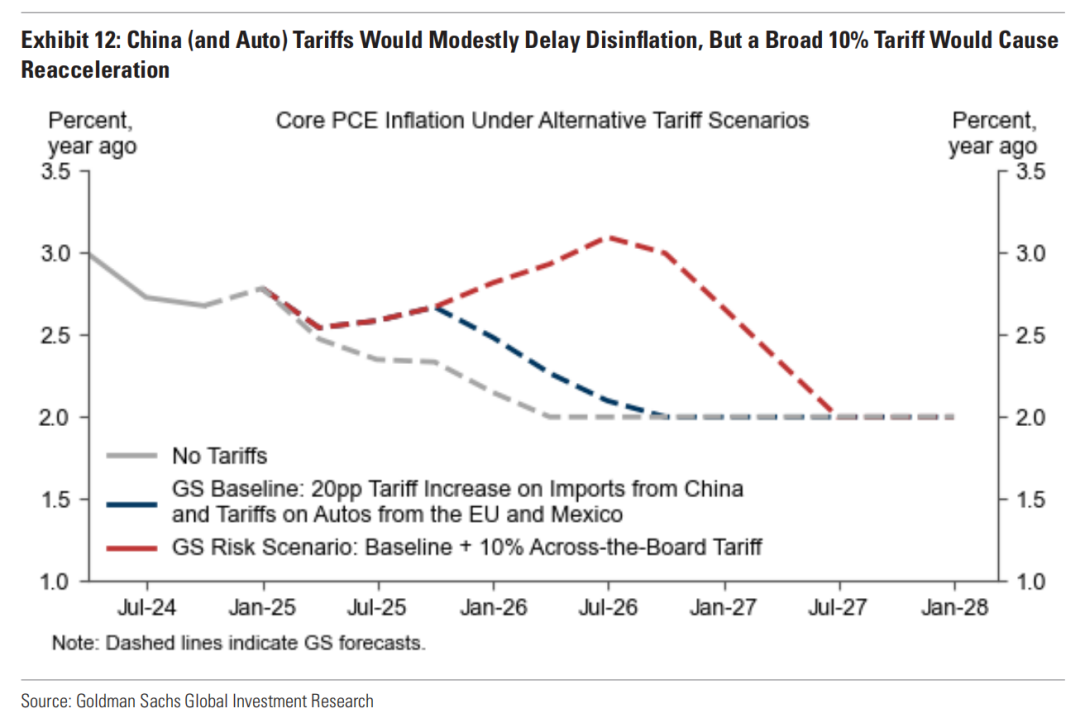

We have revised up our core PCE inflation forecast for late 2025 to 2.4%, from 2.0% before the election. Moreover, the risks are tilted to the high side because of the risk of a broader trade war. An across-the-board tariff of 10% on top of the China and auto tariffs would likely raise core inflation to 3.1% in early 2026 (Exhibit 12).

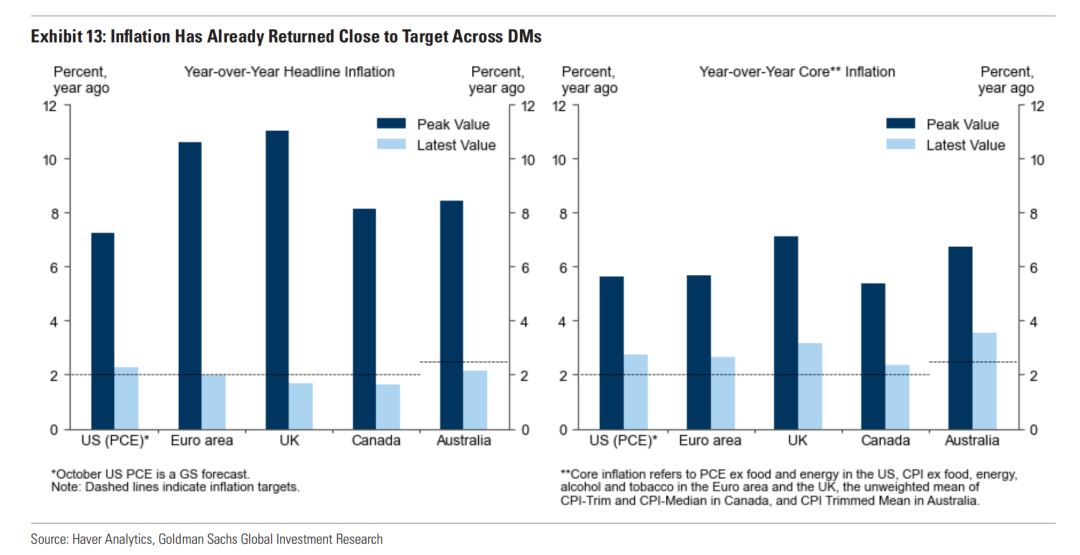

Even our revised US inflation forecast is quite benign, at least in the baseline. This is partly just an extrapolation of recent trends. Although core inflation is still modestly above target, at least on a year-on-year basis, both headline inflation and 3-month annualized core inflation are close to (and in several cases below) target across most major DM economies. Australia is a high-side outlier, but it’s worth remembering that the RBA pursues a higher 2-3% inflation target vs. 2% for most other central banks (Exhibit 13).

回顾通胀下降的波动路径

我们将2025年底美国核心个人消费支出(PCE)通胀率的预测从2.0%上调至2.4%。此外,由于更广泛贸易战的可能性,通胀风险偏向上行。如果在中国商品和汽车关税基础上加征10%的全面关税,核心通胀可能在2026年初升至3.1%(见图表12)。

即使经过修订,我们的美国通胀预测在基线情景下依然相对温和。这在一定程度上是对近期趋势的延续。尽管核心通胀仍略高于目标(按同比计算),但在多数主要发达经济体中,整体通胀和3个月年化核心通胀已接近甚至低于目标。在这一背景下,澳大利亚是一个高位例外,但需要注意的是,澳大利亚央行(RBA)追求的是2-3%的通胀目标,高于其他央行通常设定的2%目标(见图表13)。

There are also strong fundamental reasons to expect core inflation progress to continue. Aside from a direct tariff boost in the US, core goods inflation should remain low due to continued growth in Chinese exports and inventory normalization in Europe. Meanwhile, shelter inflation should continue to cool, particularly in the US where market rent indicators have looked benign for nearly two years but the official measures are only gradually catching up with reality (Exhibit 14).

核心通胀有望持续改善,这背后有多方面的基本面支撑。尽管美国可能因直接关税上调面临一定压力,但核心商品通胀预计将保持低位,这得益于中国出口的持续增长以及欧洲库存的逐步正常化。

同时,住房通胀预计将继续放缓,尤其是在美国。过去近两年中,美国的市场租金指标已经呈现温和趋势,但官方统计数据的调整仍在逐步追赶实际情况(见图表14)。

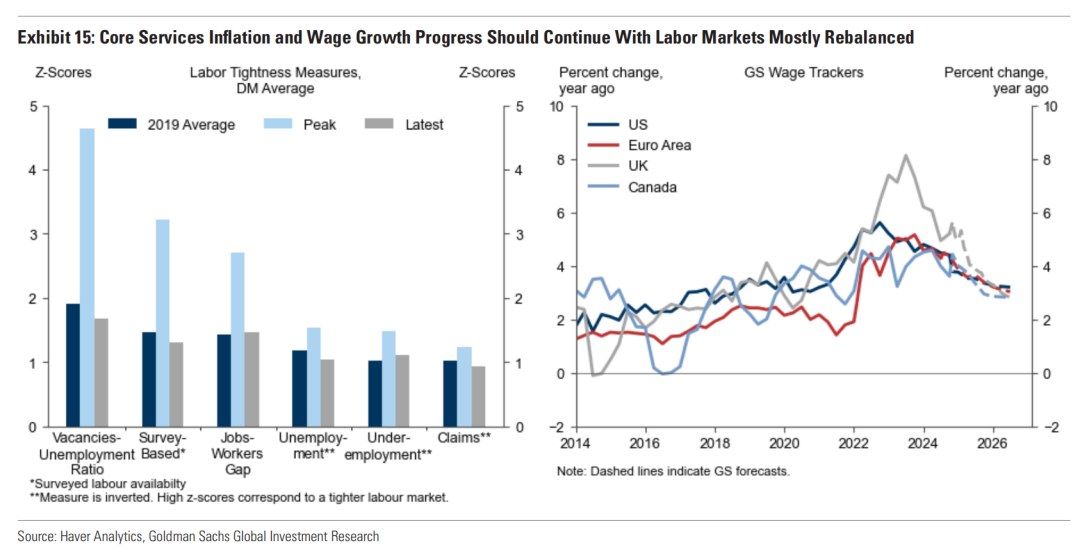

Most importantly, services ex energy and housing—which make up well over half of the core indices—are particularly sensitive to labor costs. It is therefore reassuring that a broad set of labor market tightness measures across advanced economies have returned to pre-pandemic levels. For now, wage growth remains somewhat above the pace compatible with target-consistent inflation assuming productivity grows in line with the long-term trend. However, much of the remaining gap reflects lags in the catch-up of negotiated wages to the earlier price surge, and we expect steady further wage disinflation in 2025 (Exhibit 15).

最重要的是,剔除能源和住房的服务类项目——它们占核心通胀指数的一半以上——对劳动力成本尤为敏感。因此,令人欣慰的是,发达经济体的多项劳动力市场紧张程度指标已恢复至疫情前水平。

目前,工资增速仍略高于与目标一致的通胀水平所需的增速(假设生产率与长期趋势一致增长)。然而,这一差距的大部分反映了谈判工资对早期价格上涨的滞后反应。我们预计,在2025年,工资增速将继续稳步下降,从而带来工资通胀的进一步缓解(见图表15)。

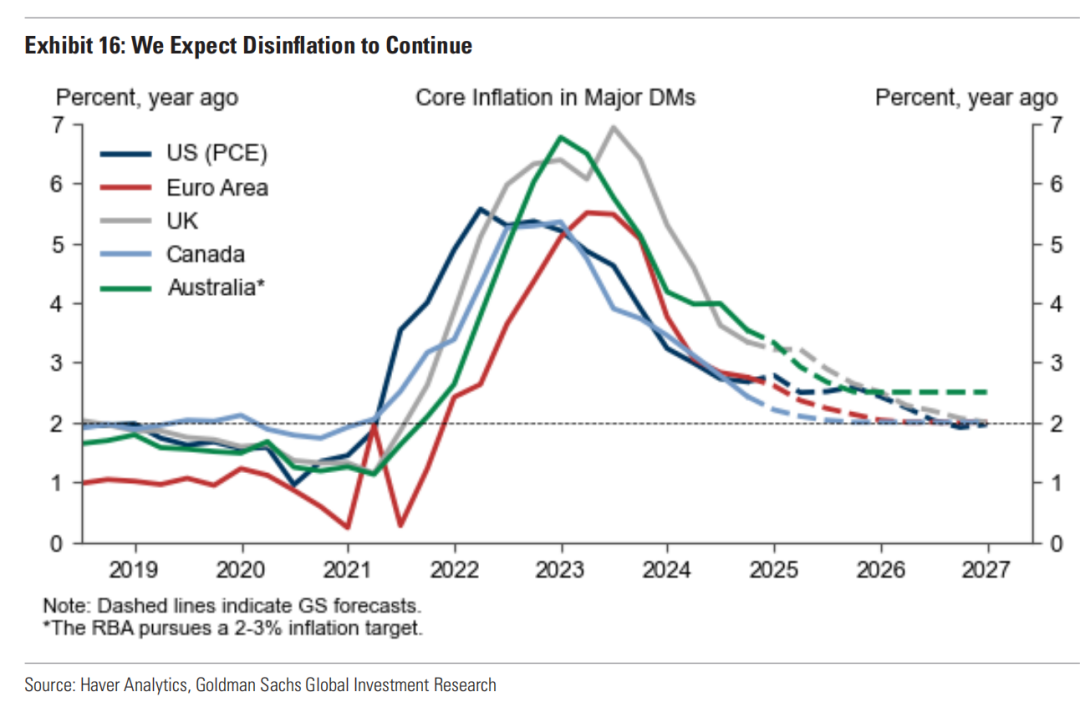

Thus, both the recent numbers and the fundamentals point to further across-the-boarddisinflation, as shown in Exhibit 16. While we expect the Euro area and Canada toreturn fully to 2% by late 2025, the US, the UK, and Australia are likely to cluster around2½%, with additional declines in 2026 likely. The inflation surge of 2021-2022 is nowfirmly in the rearview mirror.

无论是近期数据还是基本面,都表明通胀将在各领域持续回落(见图表16)。我们预计,欧元区和加拿大的通胀将在2025年底全面回归2%的目标水平,而美国、英国和澳大利亚的通胀可能保持在2.5%左右,并有望在2026年进一步下降。

2021-2022年的通胀高峰如今已成为历史,全球通胀回归正常水平的趋势愈加清晰。

Further Gradual Rate Cuts Ahead

Against this backdrop, we do not expect the US election outcome to derail the policy normalization process that is currently underway, and see most major central banks easing significantly further through 2025.

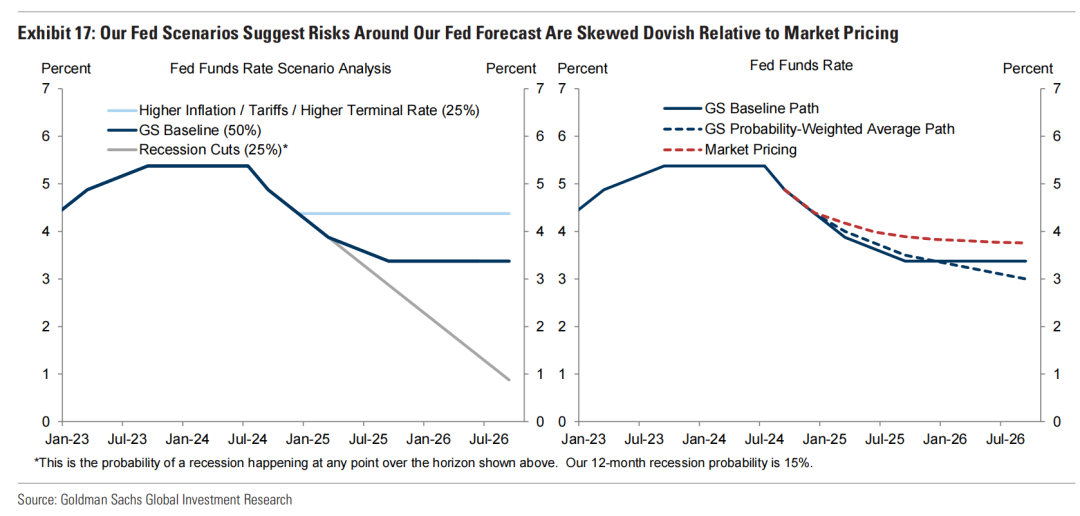

We forecast that the Fed will cut to 3.25-3.5% with sequential moves through Q1 and a slowdown thereafter. If anything, the threat of a near-term growth drag from tariffs and the Fed leadership’s continued preference for frontloaded policy normalization have strengthened our confidence in sequential cuts through early next year. While the pace after Q1 and ultimate stopping point—which may depend on the Fed’s willingness to respond preemptively to future inflation boosts from President-elect Trump’s policies—admittedly remain uncertain, our baseline and probability-weighted Fed forecasts are meaningfully more dovish than current market pricing (Exhibit 17).

未来将迎来进一步的渐进降息

在当前经济背景下,我们认为美国大选结果不会中断正在进行的政策正常化进程,预计大多数主要央行将在2025年大幅放松货币政策。

我们预测,美联储将在2025年第一季度之前采取连续降息行动,将利率降至3.25%-3.5%。此后,降息步伐将有所放缓。事实上,关税可能对短期增长造成拖累的风险,加之美联储领导层对前置式政策正常化的偏好,增强了我们对明年初持续降息的信心。

尽管第一季度以后的降息节奏及最终利率水平仍存在不确定性,可能取决于美联储是否愿意针对当选总统特朗普的政策可能引发的未来通胀上升提前应对,但我们的基线预测和加权概率预测显著比当前市场定价更偏鸽派(见图表17)。

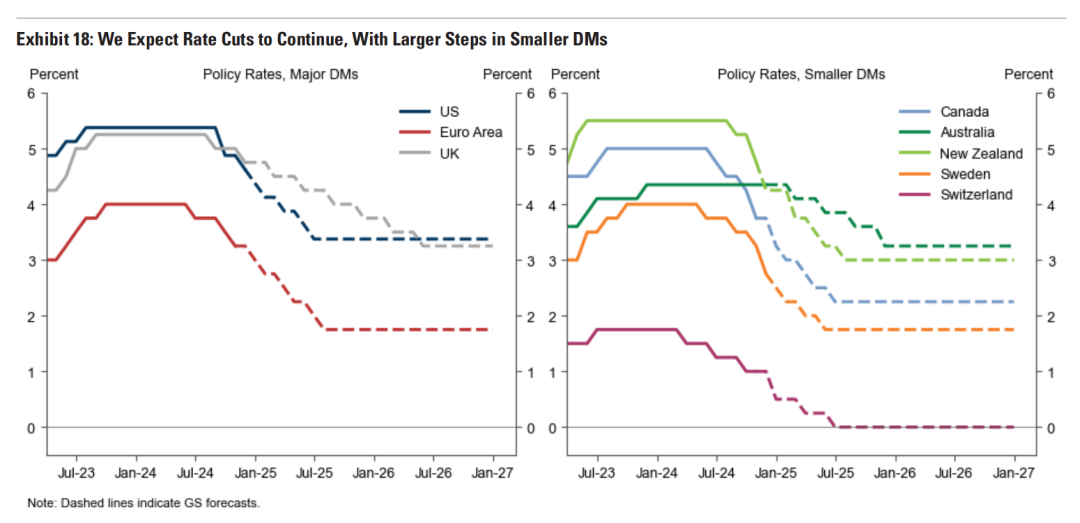

Exhibit 18 shows our policy forecasts for other DMs. In the Euro area, we continue to expect sequential ECB cuts and have lowered our terminal forecast to 1.75% on the back of our growth downgrade. In the UK, we are raising our BoE forecast to reflect a better growth outlook following a more expansionary Autumn Budget, and now expect quarterly cuts back to 3.75% by end-2025 and a terminal rate of 3.25% in 2026Q2. We continue to see risks of faster UK cuts if near-term growth disappoints, however, and our terminal rate forecast remains well below market pricing.

We generally expect more aggressive cuts in smaller DM central banks where inflation progress is even more convincing and unemployment rates have risen more meaningfully. The BoC, RBNZ, and Riksbank have already delivered 50bp cuts, and we anticipate the BoC, RBNZ, and SNB will each cut by 50bp at their next meetings. The exception among smaller DMs is Australia, where we continue to expect quarterly rate cuts starting in February. But even here we see risks as skewed dovish given that growth remains weak and inflation indicators aren’t that different from other DMs where cutting cycles are well underway

其他发达市场央行的政策展望

如图表18所示,我们对其他发达市场(DM)的货币政策预测如下:

在欧元区,我们预计欧洲央行(ECB)将继续采取连续降息措施,并基于经济增长预期下调,将终端利率预测下调至1.75%。在英国,由于更具扩张性的秋季预算改善了增长前景,我们上调了对英国央行(BoE)的预测,预计到2025年底每季度降息至3.75%,并在2026年第二季度达到3.25%的终端利率。然而,如果短期增长表现不及预期,英国降息的步伐可能会更快,我们的终端利率预测仍显著低于市场定价。

我们预计在通胀下降更明显、失业率显著上升的小型发达市场央行中,降息步伐将更加激进。例如,加拿大央行(BoC)、**新西兰央行(RBNZ)和瑞典央行(Riksbank)已实施了50个基点的降息,我们预计这些央行将在下次会议上再次降息50个基点。此外,我们预计瑞士央行(SNB)**也将采取类似措施。

澳大利亚是一个例外。尽管我们预计澳洲联储(RBA)将在明年2月开始每季度降息,但由于增长疲软且通胀指标与其他已经启动降息周期的发达经济体相差无几,澳大利亚的政策风险仍偏向鸽派。

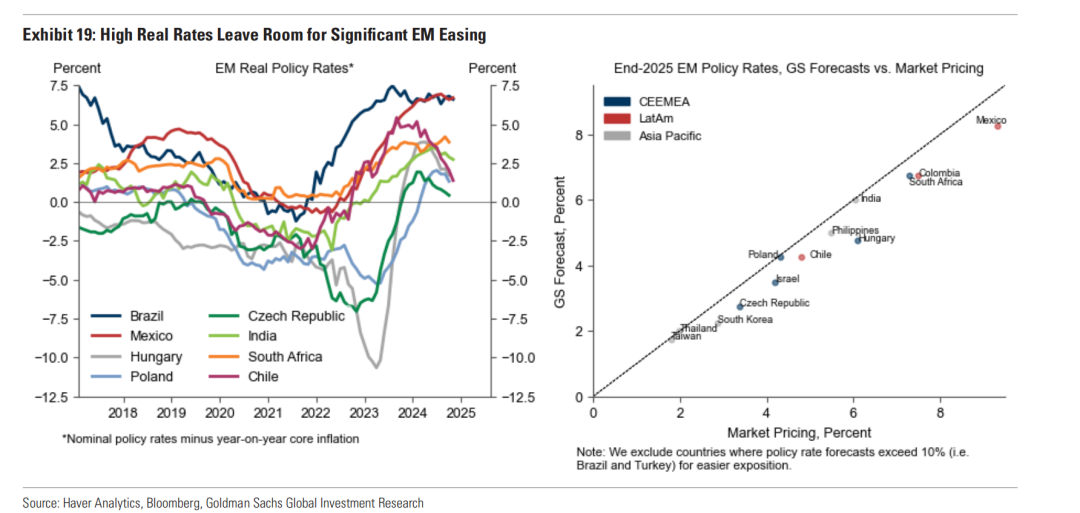

We see significant room for monetary easing in EMs as well given that policy rates remain far above neutral (Exhibit 19). This is especially true in Latin America and CEEMEA, but we also expect rate cuts to broaden in Asia over the next few quarters. The main exception to our forecast for EM rate cuts is Brazil, where we anticipate an overheated economy will prompt another 150bp in rate hikes through 2025Q1 (to 12.75%) followed by 125bp in rate cuts (to 11.50%) by end-2025. Our EM policy rate forecasts are quite dovish relative to market pricing.

我们认为,新兴市场(EM)也有显著的货币宽松空间,因为当前政策利率仍远高于中性水平(见图表19)。这一趋势在拉丁美洲和中东、东欧和非洲地区(CEEMEA)尤为显著,同时我们预计未来几个季度亚洲的降息范围也将进一步扩大。

然而,巴西是一个例外。我们预计由于经济过热,巴西央行将在2025年第一季度前再加息150个基点(将利率提高至12.75%),随后在2025年底前降息125个基点(将利率下调至11.50%)。我们的新兴市场政策利率预测相比市场定价明显更偏鸽派。

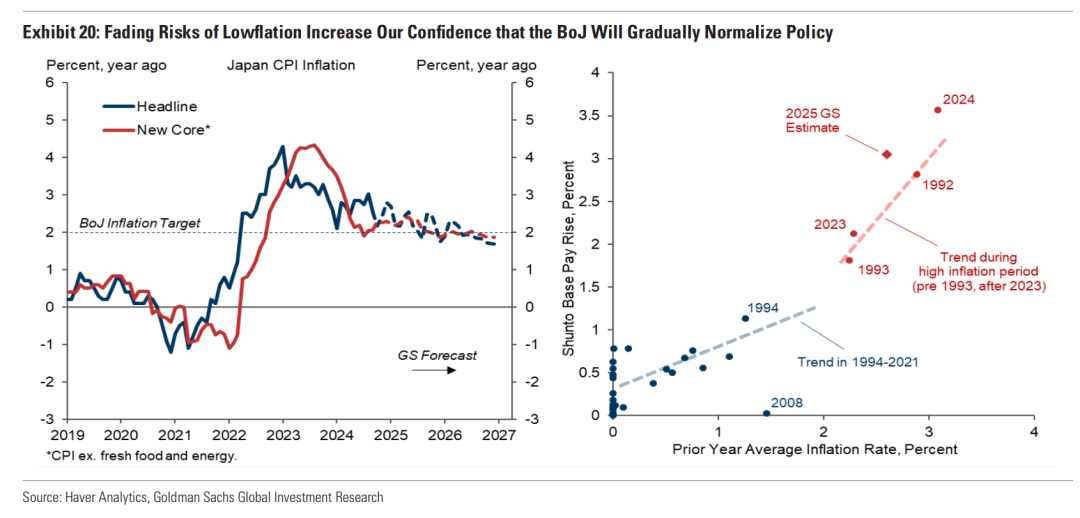

The main outlier to our forecast for steady rate cuts is Japan. A pickup in inflation and wage growth after three decades of anemic price pressures allowed the BoJ to exit negative interest rate policy in March and hike again in July. We are increasingly confident lowflation risks are behind us and rate hikes will continue. Wage growth should remain firm (we forecast a 3-3.5% base pay increase in spring 2025’s shunto wage negotiations) and is increasingly correlated with price increases, suggesting that a virtuous wage-price spiral that will help anchor inflation expectations has emerged. In addition, demand looks more robust and policy space has increased relative to the recent past, suggesting less downside inflation risk in the event that activity weakens. We expect that new core CPI (ex fresh food and energy) will increase by 2.1% year-over-year in 2025 and 2.0% in 2026 on an annual average basis, a target-consistent pace that supports our forecast for 25bp semi-annual hikes to 0.75% by end-2025 and a terminal rate of 1.5% in 2027 (Exhibit 20).

日本货币政策的特例

与我们对其他经济体普遍降息的预测不同,日本是一个显著的特例。由于经历了三十年低迷价格压力后的通胀和工资增长回升,日本央行(BoJ)在3月结束负利率政策,并在7月再次加息。我们对低通胀风险已成为历史的信心不断增强,预计日本将继续加息。

工资增长预计将保持强劲,我们预测2025年春季“春斗”工资谈判中的基本工资涨幅为3%-3.5%。与此同时,工资增长与价格上涨的关联性正在增强,这表明一个良性的工资-价格螺旋正在形成,有助于稳定通胀预期。此外,需求表现更为稳健,政策空间也较近期显著扩大,这表明即便经济活动减弱,通胀下行风险也较小。

我们预计,日本的新核心CPI(剔除生鲜食品和能源)将在2025年实现同比增长2.1%,在2026年实现年均增长2.0%,这一符合目标的通胀水平支持我们的预测,即日本央行将在2025年底通过每半年

加息25个基点将利率提升至0.75%,并在2027年达到1.5%的终端利率(见图表20)。

Better US Growth but Better Market Pricing

Our baseline economic forecast for steady growth, cooling inflation, and further non-recessionary rate cuts, as well as policies that could be helpful to corporate earnings, represents a friendly risk asset backdrop for 2025. This view, alongside our economic forecast for continued US outperformance is reflected by our baseline 2025 market forecasts.

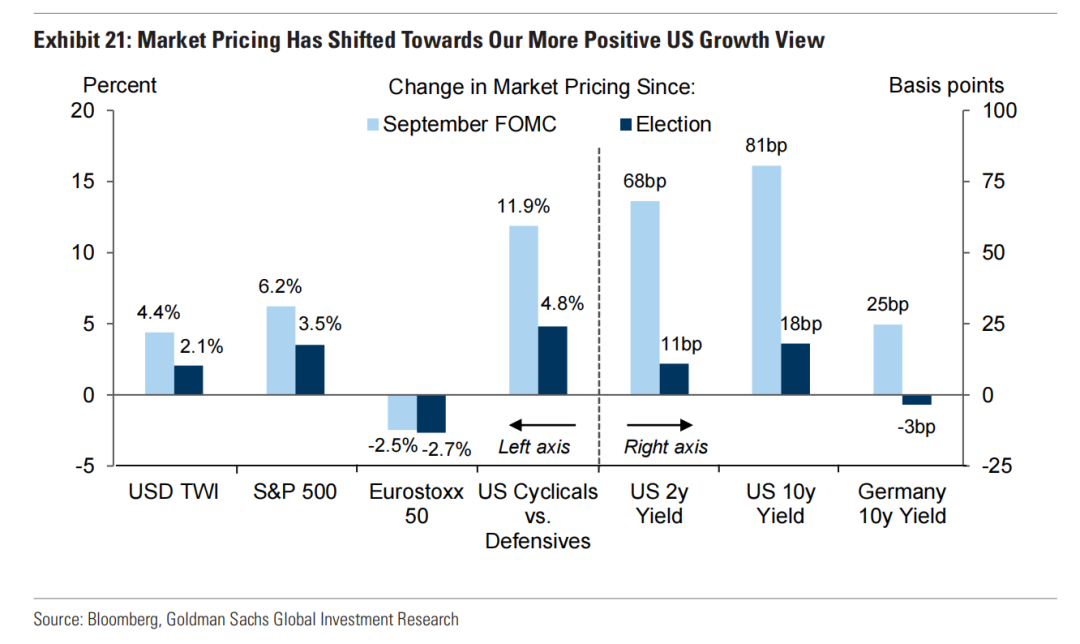

A key challenge, however, is that markets have already moved a long way to price this kind of outlook. Our US growth view is once again well above the consensus forecast. But both ahead of and since the election, investors have sharply upgraded the US growth views embedded in assets, pushing US equities and the USD to fresh highs and widening the gap between US and European bond yields (Exhibit 21). We think our baseline forecasts still justify higher equity prices and further USD outperformance, but that judgment is more finely balanced than it was. As US markets take more credit for favorable policies up front, the risk of ultimate disappointment will rise.

美国经济增长更强劲,但市场定价更充分

我们的基线经济预测表明,稳定的经济增长、通胀回落和非衰退性的进一步降息,以及有利于企业盈利的政策,将为2025年的风险资产提供友好的环境。这一观点与我们对美国经济持续领先的预测一致,并体现在我们2025年的基线市场预测中。

然而,市场定价已在很大程度上反映了这一前景。这是一个关键挑战。尽管我们的美国经济增长预测仍显著高于市场共识,但在大选前后,投资者对资产价格中反映的美国增长预期进行了大幅上调,推动美国股市和美元创下新高,并进一步扩大了美欧债券收益率之间的差距(见图表21)。

我们认为,基线预测仍支持更高的股价和美元的进一步走强,但与之前相比,这一判断已更为谨慎。随着美国市场在早期充分消化了政策利好,最终令人失望的风险也将随之上升。

Because the market has moved much closer to our central case, our forecasts for many key assets are not far from current levels. The modest positive returns that we expect for many assets come more from the yield or carry than a big shift in spot prices. This means that the investing backdrop is likely to depend on the distribution around that base case even more than usual. The US election outcome widens the distribution of policy shifts. The core challenge continues to involve maintaining some exposure to a robust US economic outlook, while protecting against the key tail risks.

由于市场定价已经非常接近我们的基线预测,我们对许多关键资产的预测值与当前水平相差不大。我们预计,许多资产的温和正回报更多来自于收益率或持有收益,而非现货价格的大幅变动。这意味着,投资背景可能会比以往更依赖基线预测周围的分布情况。

美国大选结果扩大了政策变化的分布范围,进一步增加了不确定性。核心挑战在于如何保持对美国经济强劲前景的适度敞口,同时规避关键尾部风险。

Tail Risks Now a Critical Focus

The potential for a broader trade war looms large among those tails. The narrowly focused tariffs that feature in our baseline scenario are likely to be less disruptive both to the US economic picture and to China’s trade and markets, given the experience since the first round of tariffs in 2018-2019 and China’s reduced trade exposure to the US. As in 2019, the actual announcement of tariffs could still move markets, including China’s currency. But expectations of action on this front are high and markets are relatively well-prepared for these outcomes.

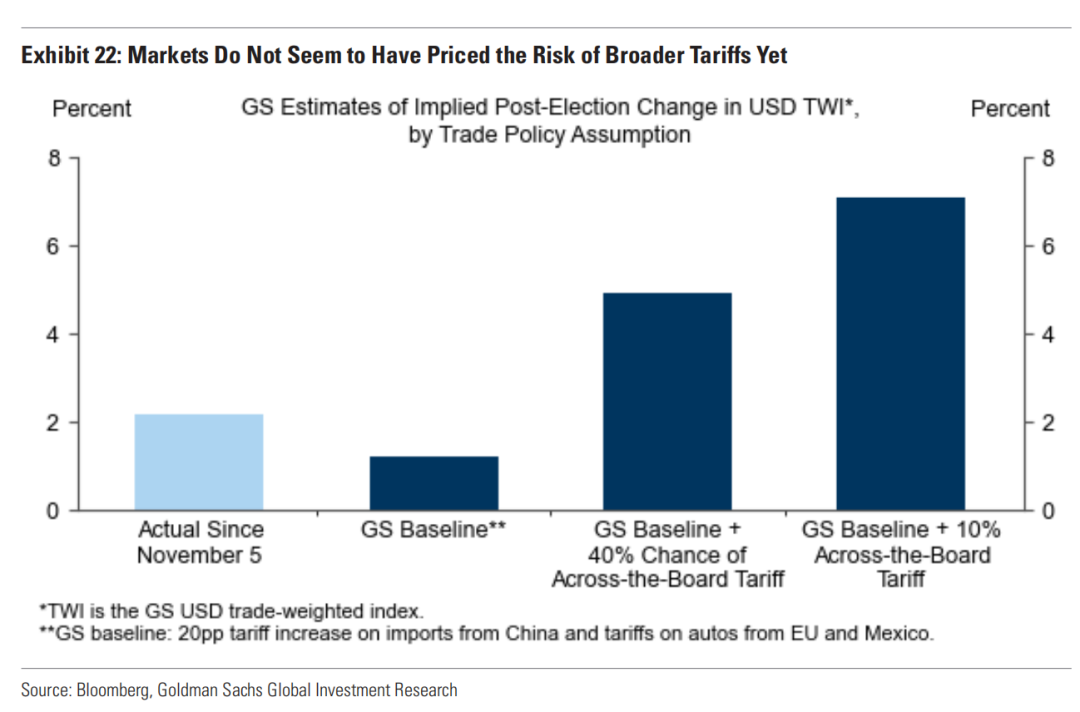

We think the impact of a broader across-the-board tariff is underpriced, particularly for its potential impact on Europe and some non-China EM economies (the incremental pressure on China should be relatively smaller given that tariffs are already expected). We think a firmer shift in this direction could lead to meaningful further USD upside (Exhibit 22) and add to downward pressure on non-US equities and bond yields. Our baseline forecast is already one in which European GDP growth is below consensus and European yields and EUR/USD decline further. A broader trade war would add to those pressures. The impact on US markets is less certain, but we think across-the-board tariffs and the threat of retaliatory action could weigh on US equities too and might ultimately push US yields lower, as it did in 2019.

尾部风险成为关键关注点

全面贸易战的可能性在当前尾部风险中尤为突出。在我们的基线预测中,影响范围较小的针对性关税对美国经济、中国的贸易与市场的干扰相对有限。这一点已在2018-2019年首轮关税中得到验证,且中国对美贸易依赖已显著下降。与2019年类似,关税的实际宣布仍可能对市场产生影响,包括对人民币汇率的冲击,但由于市场对这一前景已有较高预期,相关应对措施已较为充分。

相比之下,市场对全面性关税的潜在影响存在低估。特别是这一政策可能对欧洲及部分非中国的新兴市场经济体造成更大压力(相较之下,中国所受的增量压力会较小,因为市场已预期部分关税政策)。如果政策更明确地向这一方向转变,我们预计将进一步推动美元显著走强(见图表22),并对非美股市和债券收益率施加更多下行压力。

在我们的基线预测中,欧洲GDP增长已低于市场共识,欧洲债券收益率和欧元兑美元汇率(EUR/USD)也呈进一步下降趋势。全面贸易战将加剧这些压力。对美国市场的影响则不确定性较大,但我们认为,全面性关税及其可能引发的报复行动,将对美股构成压力,并可能最终使美国债券收益率进一步下降,类似于2019年的情况。

In other areas, we think the risks are more balanced. The US election has clearly increased the possibility of additional fiscal expansion and fresh focus on the sustainability of the US public debt profile. But our central scenario of only modest fiscal stimulus makes us more skeptical that we will see a sharp increase in fiscal risk premium in US Treasury markets. Even in the UK, where the market has worried more in the light of the recent budget, we would look to fade those risks in both rates and currency markets. Given our robust US growth views, the bigger upside risk may simply be an earlier stopping point to the Fed easing cycle, which could prompt markets to judge that the neutral rate is higher than we are assuming. It is only in Japan where our baseline policy path lies well above the market and where we expect bonds to underperform. Near-term inflation risks are also two-sided, after a sharp move higher in market pricing of US inflation over the next couple of years. Short-dated US inflation swaps are priced well above our US inflation forecast, so we think this is one area of the market that already reflects a meaningful chance of broader trade risks.

Oil market tails lie in both directions too. In our baseline forecast, we expect Brent prices to stay in a $70-$85/bbl range. But the risks of breaking that range are growing. In the short term, the new administration raises the risks to Iranian supply, which have already been elevated due to Israel-Iran conflict. That upside tail risk adds to the value of commodity longs in a portfolio context. We think the medium-term risks, however,skew to the downside of our forecast range. That is both because ample supply is still being kept off the market which could begin to find its way back into the system in 2025, but also because broader-based tariff action could hurt global demand. In those scenarios, oil prices might again become a tailwind for disinflation trends.

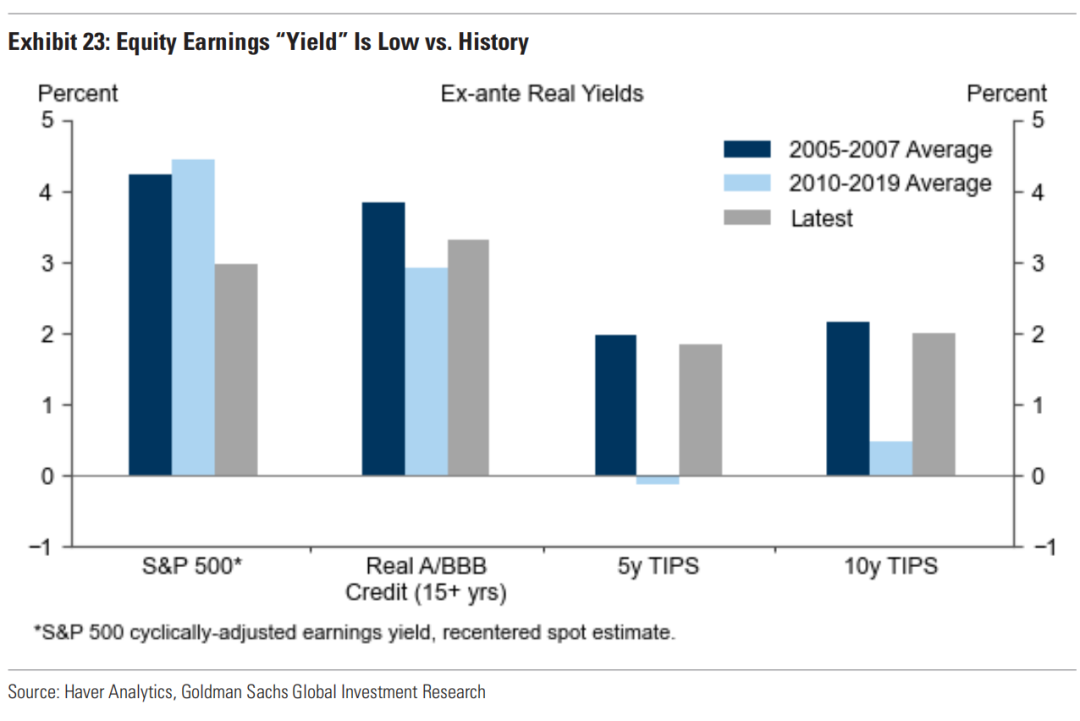

High Valuations Fatten the Downside

High valuations reinforce the importance of focusing on these tail risks. US equity valuations are now at levels that have not been exceeded in the post-war era except in the late 1990s. Some of the recent uplift comes on expectations that upcoming policies will boost after-tax earnings. But even adjusting for this, US equity valuations look historically high (Exhibit 23). Credit spreads too are near their historical lows, and even those segments of the market that were pricing more elevated risk premium have now compressed. As our Portfolio Strategy team recently showed, the long-term expected returns from equities now look low as a result (they estimate 3% nominal returns over the next decade when accounting for the risks from unusually high market concentration). As a result, prospective returns on government bonds and credit on that longer horizon look relatively better, reflecting historically low levels of the Equity Risk Premium and Equity-Credit Premium.

风险均衡与高估值下的市场动态

在其他领域,我们认为风险更加均衡。美国大选显然增加了进一步财政扩张的可能性,同时也引发了对美国公共债务可持续性的关注。然而,我们的基线预测是仅有温和的财政刺激,因此我们对美国国债市场的财政风险溢价大幅上升持更怀疑的态度。即使是在市场对英国预算更为担忧的情况下,我们仍然倾向于淡化利率和汇率市场中的相关风险。

考虑到我们对美国经济增长的强劲预期,更大的上行风险可能在于美联储降息周期的提前结束,这可能促使市场判断中性利率高于预期。而在日本,我们的基线政策路径明显高于市场预期,因此我们预计日本债券表现将相对较差。

短期通胀风险也存在两面性。尽管未来几年市场对美国通胀的定价大幅上升,但短期通胀互换的价格已远高于我们的通胀预测,这一市场板块可能已反映了更大范围的贸易风险可能性。

原油市场的尾部风险同样存在双向性。我们基线预测中的布伦特油价将维持在70-85美元/桶的区间,但突破这一区间的风险正在上升。短期内,新政府可能加剧伊朗供应风险,尤其是在当前以色列-伊朗冲突的背景下。这种上行尾部风险提升了大宗商品多头在投资组合中的价值。然而,从中期看,风险更偏向下行,这不仅是因为充足的供应可能在2025年重新进入市场,还因为更广泛的关税行动可能打压全球需求。在这种情景下,油价可能再次成为通缩趋势的推动因素。

高估值放大下行风险

高估值使得关注尾部风险更加重要。目前,美国股市估值已达到二战后仅在1990年代末被超过的水平。尽管近期的上涨部分源于对政策将推动税后收益的预期,但即使在调整这一因素后,美国股市的估值仍处于历史高位(见图表23)。

同时,信用利差接近历史低点,即使是此前定价较高风险溢价的市场板块也出现了明显压缩。正如我们投资组合策略团队近期所示,长期来看,这使得股票的预期回报较低(预计名义回报率在未来十年仅为3%,考虑到市场异常高的集中度带来的风险)。因此,在更长的时间跨度上,政府债券和信用资产的预期回报相对更具吸引力,反映了股票风险溢价和股票-信用溢价的历史低水平。

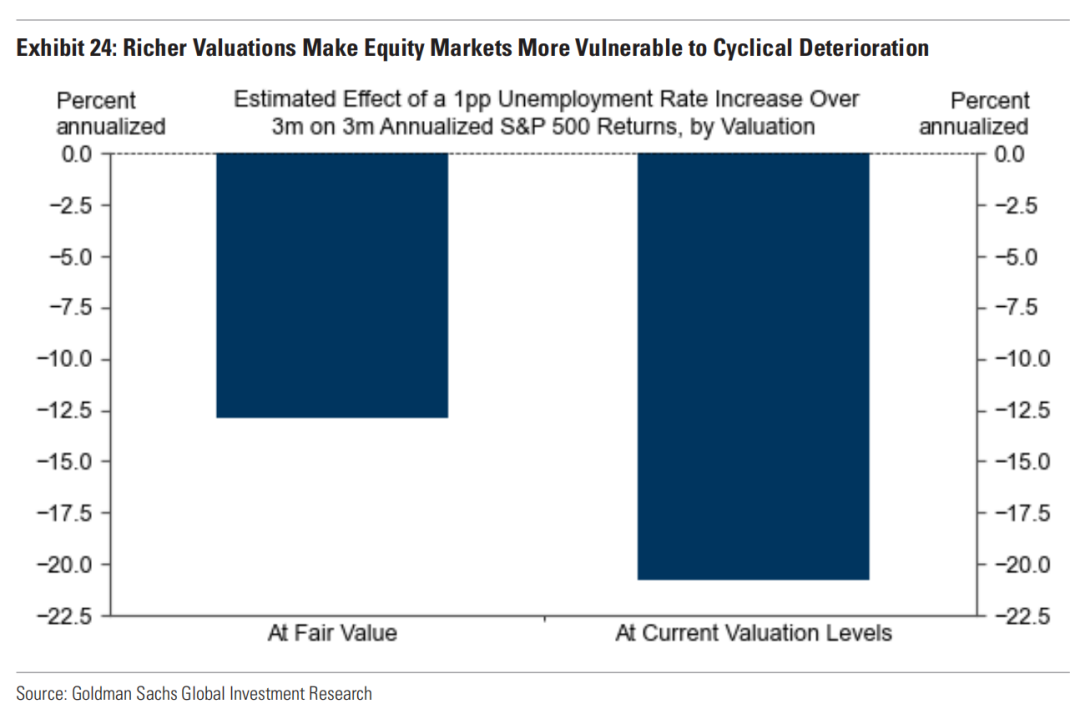

Rich valuations are not an obstacle to further equity gains if the cyclical tailwinds are powerful, as we have seen already in 2024. For US equities, we find that the price for higher valuations is often paid disproportionately when the cycle deteriorates (Exhibit24). Our baseline forecast means that challenge will most likely be avoided in 2025. But if growth risks do rise more sharply than we anticipate, equity downside could be faster and deeper than normal. The sharp drops in risk assets, and spikes in volatility, in early August may be a harbinger of that kind of sensitivity. That fatter downside tail also highlights the importance of keeping an eye on another kind of “valuation challenge”—the point at which our more optimistic macro forecasts seem fully reflected in assets. As in 2024, we are likely to push harder on our asset views when the market is clearly in doubt about elements of our macro picture.

高估值与周期性尾部风险的权衡

高估值并不一定阻碍股市进一步上涨,前提是周期性利好因素足够强劲,正如我们在2024年所见。然而,对于美国股市而言,高估值带来的代价往往在经济周期恶化时表现得尤为显著(见图表24)。根据我们的基线预测,这一风险在2025年很可能得以避免。但如果增长风险超出预期显著上升,股市下行可能比正常情况更快且幅度更大。

2024年8月初风险资产的剧烈下跌和波动率飙升可能预示了市场对这种敏感性的反应。这种更大的下行尾部风险也突显了关注另一种“估值挑战”的重要性——即我们更乐观的宏观预测是否已经被资产价格充分反映。当市场对我们的宏观图景中的某些要素存在明显疑虑时,正如2024年的情况,我们可能会更积极地调整我们的资产观点。

Maintain Exposure, Limit Tails

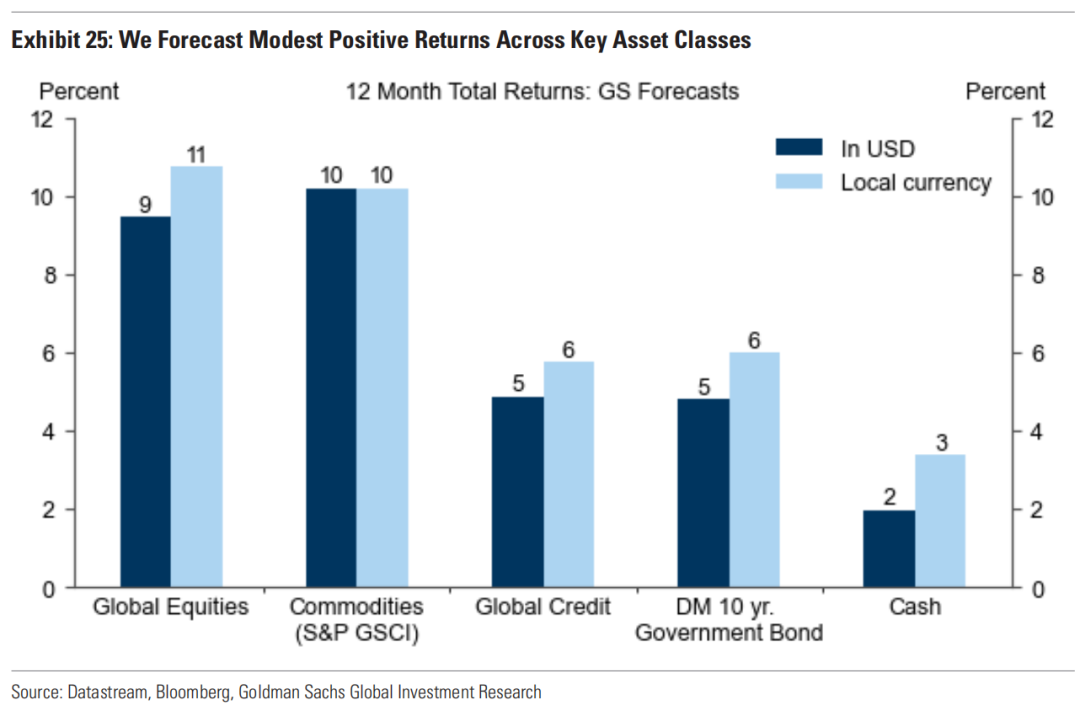

Although markets have already moved to reflect key elements of our macro view, we still forecast modest positive returns across the key asset classes (Exhibit 25). US growth resilience should still support outperformance of US equities and

underperformance of US bonds, alongside some further expected upside to the US dollar. Given subdued valuations, EM equities are likely to outperform fixed income.And while EM hard currency fixed income should prove more defensive than local currency in a strong USD environment, local currency assets have more scope to perform if the tails are avoided. Commodity markets should continue to benefit from a positive roll return, with lower contribution from price shifts.

保持敞口,控制尾部风险

尽管市场已经反映了我们宏观观点中的关键要素,但我们仍然预测主要资产类别将实现温和的正回报(见图表25)。美国经济的韧性预计将继续推动美国股市表现优于其他市场,而美国债券表现逊色,同时美元可能进一步走强。

在估值较低的背景下,新兴市场(EM)股票可能表现优于固定收益资产。尽管在美元走强的环境下,新兴市场的硬通货债券预计比本地货币资产更具防御性,但如果尾部风险得以规避,本地货币资产有更多的表现空间。

此外,大宗商品市场预计将继续从正的展期收益中受益,但价格变动的贡献将较低。

The key challenge is to maintain exposure to these themes, while limiting the major tail risks. Diversification can help address some of these challenges. The ongoing decline in inflation across a range of economies in 2024 has allowed central banks, including the Fed, to focus more on the risks to growth. We see risks from both growth and inflation/policy shocks, particularly in the next few months as the Trump policy agenda takes shape. But although the market may still oscillate between these different risks,we think the correlation of bonds and equities is more likely to drift lower than higher over the medium term. This means that US Treasuries, and even more so Bunds and Gilts, can still play an important diversifying role in portfolios. TIPS too look appealing since real yields have room to fall if growth disappoints, but inflation protection remains valuable. Broadening US equity exposure towards mid-cap equities or a more equal-weighted allocation may mitigate concentration and valuation risks. Long USD positions should also provide protection against both US rate upside and broadening tariff risks, reinforcing the case for US investors to keep hedging their overseas bonds (and equity) exposures.

As in 2024, we think there are strong arguments for using options to provide protection against macro tails. Equity volatility has fallen post-election and this makes it easier to gain upside exposure to US assets through call options again. Deeper downside exposure (including in European equities which are vulnerable to some key risks) also looks more attractively priced. Long USD optionality remains appealing (especially against EUR, CAD, SGD and KRW), while upside in gold and oil can still protect against some key tails. Some assets could also benefit if US policy risks fail to materialize. In 2017, the first year of the first Trump administration, EM stocks and currencies ultimately outperformed. A more restrained US fiscal impulse, or a more narrowly focused trade agenda, could again provide relief to parts of the EM universe where those risks have been most clearly reflected. Some exposure to that kind of upside may be useful too.The wider range of potential market outcomes means that any declines in volatility across assets in 2025 are likely to be opportunities to add hedges.

关键在于保持敞口并限制尾部风险

维持对核心投资主题的敞口,同时有效控制尾部风险,是当前投资策略的主要挑战。多元化是应对这些挑战的一个重要工具。2024年通胀在多国持续回落,使包括美联储在内的央行得以更加关注增长风险。我们认为,未来几个月中,随着特朗普政策议程的逐步成型,市场将面临来自增长和通胀/政策冲击的双重风险。尽管市场可能在不同风险之间反复震荡,但我们预计债券与股票的相关性在中期内更可能降低而非提高。因此,美国国债(尤其是德国国债和英国金边债券)仍是投资组合中重要的多元化工具。

同时,TIPS(通胀保值债券)也具备吸引力,因为在增长令人失望的情况下,实际收益率可能下降,而通胀保护仍然具有价值。为了减少集中化和估值风险,将美国股票敞口拓展至中型股或采用更均衡的配置方式可能更为有效。此外,持有美元多头头寸可以对冲美国利率上行和关税扩大风险,进一步支持美国投资者对海外债券和股票敞口进行套期保值。

通过期权保护尾部风险的策略在2024年已被证明有效,而这一策略在2025年仍具吸引力。大选后股票波动率下降,使得通过看涨期权再次获得美国资产的上行敞口变得更为容易。而对于更深度的下行风险(如欧洲股票因一些关键风险的脆弱性),期权价格也显得更具吸引力。美元期权多头(特别是针对欧元、加元、新加坡元和韩元)仍值得持有,而黄金和原油的上涨潜力则可对冲部分关键尾部风险。

一些资产可能在美国政策风险未能兑现时受益。例如,2017年第一届特朗普政府执政的第一年,新兴市场的股票和货币表现优异。如果美国财政刺激力度较小,或贸易议程更加集中化,新兴市场中风险反映最显著的部分可能再次得到缓解。在投资组合中适度配置这类潜在的上行机会也具有一定意义。

更广泛的市场结果区间意味着,2025年资产波动率的任何下降可能是增加对冲头寸的良机。